(Update 9/28/25) Since I wrote this, Javier Milei is taking a $20 billion bridge loan from Trump, which to me strengthens my argument relating to the dollarization of Argentina.

According to Newsweek, “Trump Admin’s $20 Billion ‘Bail Out’ for Argentina’s Milei Raises Eyebrows” (Published Sep 25, 2025 at 03:06 PM EDT, updatedSep 25, 2025 at 04:17 PM EDT0:12), by Mandy Taheri.

“The Trump administration says it is working to provide tens of billions of dollars to Argentina’s President Javier Milei, in a financial bailout that many critics say clashes with President Donald Trump’s “America First” platform.The U.S. State Department told Newsweek Thursday that the America First Foreign Assistance programs must align with administration policies and advance concrete U.S. national interests.Why It MattersOn Wednesday, U.S. Treasury Secretary Scott Bessent confirmed the United States is in talks to provide $20 billion to Milei. The announcement comes months after the Trump administration dismantled the U.S. Agency for International Development (USAID) in an effort to instead support programs aligned with Trump’s “America First” agenda.” https://www.newsweek.com/trump-admins-20-billion-bail-out-for-argentinas-milei-raises-eyebrows-10780604 (End of update).

Is Milei a stooge of the global banking syndicates simply trying to implement austerity measures as a means of handing over the Argentine economy to corporations?

Is he a faux populist who is handing Argentina’s monetary policy over to the US Federal Reserve, International Bank of Settlements, etc.?

Or is Milei a genius who is making a tough short-term decision in order for Argentina to finally see sustained long term growth?

Disclaimer: I am just writing. I do not think that there is necessarily a direct correlation or grand plan to bring to life the fictional world of the book or movie Starship Troopers.

However, what is happening in Argentina does mirror – softly – what appears in the 1997 film of Starship Troopers, even if we are speaking in mere analogous terms.

Yet, approaching this post from a literal or analogy standpoint, we can still help to grow our perceptions, deconstruct history, categorize and organize data, etc., particularly pertaining to understanding fascism, racism, imperialism, etc.

One thing that is certainly real in our real world, is that there are doubts about liberal democracy, and there are demographic shifts where the Anglo post-colonial New World is merging with the Latin post-colonial New World, but there is also the eerie 1920’s or 1930’s rise of autocratic leaders.

One of my big ideas on this site is that books such as Starship Troopers by Robert Heinlein and the Ender’s Game Saga by Orson Scott Card eerily foreshadowed real world political events or attempts at alliances, etc.

So let’s talk about how Argentine President Javier Milei plans on “dollarizing” the Argentine economy.

According to Valentina Demalde (2/15/2024) of the Business Review at Berkley (BRB), “Dollarization as a potential economic strategy for Argentina presents several compelling advantages. Foremost, it promises currency stability and inflation control, a precious commodity in a nation with a history of hyperinflation and devaluation. This stability can instill trust among investors and the public, offering a predictable economic environment. With a stable U.S. dollar, Argentina may enjoy lower interest rates, a boon for businesses and individuals alike, making borrowing more affordable. Furthermore, adopting the U.S. dollar can attract foreign investment, with investors favoring countries with stable and widely accepted currencies. This influx of foreign capital can stimulate economic growth. Additionally, businesses engaged in international trade would benefit from reduced transaction costs, as they would no longer need to navigate currency exchange. Finally, dollarization can promote financial integration with the global economy, potentially increasing trade and investment in Argentina.“

“Dollarization in Argentina presents several potential drawbacks. Most notably, it entails relinquishing control over domestic monetary policy, a vital tool for governments to manage economic challenges— Milei sees this as an advantage due to a lack of trust in the government’s management. The prospect of dependence on the U.S. economy is concerning, as it would make Argentina vulnerable to U.S. economic fluctuations and shocks. However, Milei’s plan to increase trade with the U.S. aims to address this issue. Dollarization also carries a risk of exacerbating short-term social inequality, as those with access to U.S. dollars may initially benefit, although proponents like Milei argue that the long-term effects of a stable economy will ultimately improve the overall situation of society. The loss of seigniorage, while viewed as a pro by some, poses a significant drawback as it could limit the government’s capacity to fund public spending. Finally, the transition to a dollarized economy could trigger political unrest and opposition from stakeholders invested in maintaining the status quo.” [Source: https://businessreview.studentorg.berkeley.edu/javier-mileis-dollarization-vision-a-new-era-for-argentinas-economy/#:~:text=He%20emphasizes%20a%20gradual%20approach%20to%20dollarization%2C%20driven,align%20with%20the%20preferences%20of%20the%20Argentine%20population.]

Does Milei’s dollarization effort by proxy absorb Argentina into the sphere of American power and hegemony?

Yes and no.

American dollars were already in high demand in countries such as Argentina because of their purchasing power, so Milei’s idea could be argued as institutionalizing what people have already been doing out of necessity to survive.

Argentines get dollars often but not always from black market currency dealers, but since it is illegal, dealers can sell at higher rates than what banks offer to exchange, yet Argentine banks limited how much currency you could covert thus creating the black market.

Yet, even if Milei’s idea will work, there could be certain ramifications – for better or worse, once Argentina accomplishes full dollarization.

Despite having focused on economics in my undergraduate business education, I am no expert economist by any means. However, let’s logically think through somethings.

Argentine Pesos are less valuable that American Dollars, so American dollars are far more expensive to obtain.

If you have a lot of something that is near worthless and you’re trying to get something that is far more expensive, you’re only going to be able afford a smaller amount of that more expensive product.

So, dollarization seems deflationary in nature. It is essentially the argument of gold standard advocates to go back to the gold standard, but rather instead of using gold, which is truly deflationary.

There’s not enough fungible gold in the world to prop up the sheer size of the global economy as well as fund future innovation which is often funded by running government deficits as a form stimulus.

Milei is treating the US Dollar as something akin to gold.

The USD is relatively stable, people trust America’s banking system (even when it collapses on itself such as post 2008 crash), the US has the most sway over the SWIFT banking system, it has a strong military with fast striking capability that not only has strong air/space superiority but also protects the high seas where global trade happens via shipping, etc. Oil is also priced and transacted in dollars.

The United States has also affected the world as far as fashion, music, language, art, etc., where everyone on Earth is a little bit “American”.

For example, the relatively racial (not ethnic) homogenous Chinese and Russian populations do not have the cultural vigor and gravitas that the USA does (i.e., dynamism as Zbigniew Brzezinski, author of the Grand Chessboard (1997), may have said), since American culture is largely a melting pot glued together with an Anglo English (lingua franca) logos largely defined by pragmatism. India with Bollywood has more sway than any art coming from China or Russia into the West.

Yet, by deflating the money supply, there will be less money as far as volume goes.

To have more of something that is worthless, or to have less of something that is worth more?

The goal it seems to have less of something that is worth more because once you get it, you have something people are willing to transact with, thus this move could help promote future growth and investment.

It is as if he is whacking down a forest with blight, just to invest in more expensive seed and hope a healthier forest grows back sooner than later.

But dollars just won’t just fall into the lap of the Argentines.

They will have to purchase them or earn them. Or, be gifted them.

By earning them, they can sell their products (exports) and demand payment in only US dollars and then not reconvert those dollars they earn to Argentine Pesos or hold those US dollars in bank vaults but peg the circulating pesos to the number of US dollars held in reserve.

Or they can take out loans at US dictated interests’ rates and then use those dollar-backed loans to stimulate economies, hopefully make money, and use parts of their profit to pay off interests or principal payments; yet, if they do this, it could create a cyclical effect for the better, because if they are able to use those dollar based loans to stimulate economies enough to attract foreign investments, they can dictate those investment also be done in dollars, thus increasing the overall volume of US dollars in circulation, thus increase overall value of the overall economy as a whole.

Yet, the issue with borrowing US dollars (taking out loans in US dollars) is that interest rates are not historically low anymore and institutions can add on top of the base federal funds rate, i.e.., the Fed sets a base rate, but a bank may add onto that base rate to develop their Annual Percentage Rate/Annual Percentage Yield’s on consumer credit.

The United States since it has so much sway over the IMF (International Monetary Fund) which has a debt plan already with Argentina, it may be beneficial to “give” Argentina dollars since the US can print money.

In the wake of the expiration of the Petrodollar agreement between the USA and Saudi Arabia, the world is relatively calm.

I noticed watching certain stock news outlets and programs on TV, that no one talked about it.

The only people talking about it were doomsday cryptocurrency advocates, who of course want fear just like gold speculators to bolster their price of their own assets.

But, with the petrodollar scheme having expired (assuming the Saud’s won’t want to re-enter a newly negotiated agreement), the US dollar will need other means of propping up its currency in a multi-polar world where once emerging economies are rising powers such as Brazil, India, Nigeria, (outside of China) etc.

The USD is fine. If the Euro is fine, the USD is more than fine considering the global influence the US has, including already established relationships with oil producing countries who can fill the void (diversify the role) where the Saud’s left off. If anything, this move by the Sauds may move them closer to China and thus Russia, but that thus pulls them away from the Western influence they may have had, and pushes the USA closer to friendly and more conducive oil partnership nations with Norway, Canada, Mexico, Nigeria, etc.

The USA is also a net exporter of oil as well itself, and is transitioning to alternative energy sources such as lithium based EVs (which Argentina has lots of as far as lithium), nuclear power, etc. Also, in a dreamworld, the USA would have an improved relationship with Venezuela and get them to play a larger role in a new type of petrodollar role, such as them doing oil transactions in US dollars and investing excess oil into US treasuries in exchange for foreign direct investment, lifting sanctions, and debt cancellation from the USA and other international creditors. It makes no sense that Donald Trump can talk to North Korea and the conservatives don’t lambast him, but the moment someone tries to talk to Cuba, Venezuela, etc., all of a sudden you become unpatriotic.

Milei’s idea may work. Tough times will a happen as the money supply deflates (evaporates) thus hurting the working classes who need…money, even if it’s the less valuable peso. Yet, if Argentina can dollarize, the nation will de facto act like any other US territory. Argentina would likely have to enter into a free trade agreement to make it all worthwhile and better sync its economy from top-to-bottom with the United States which would include correlating its business/trading day to that of the USA; expanding sister city agreements with US cities and establishing exchange programs for students; expanding student visa agreements and entering into comprehensive research agreements with college institutions; voting in favor of the USA on international governing bodies such as the UN; entering in mutual security and law enforcement pacts; implementing more stringent US food and safety standards on consumer goods and foods, and possibly even permitting the US to house troops in Argentina to conduct joint-exercises (which could be a way of bridging any historical tensions between Argentina and the British), etc. We already have Messi in Miami… This sounds cheesy but a big part of diplomacy is sports, culture, etc.

If so, in a weird way, this sort of goes back to my “Starship Troopers” theory I have written about earlier, which is essentially how Starship Troopers is happening notably the Hispanicization of the USA, Argentina’s role in the 1997 film of Starship Troopers (and its real-world history of fascism), the militarization of feminism to support the Military Complex. Also, my Starship Trooper’s thesis involves rising tensions with China, exacerbated by the Trump Administration’s Steve Bannon of the Council on National Policy and this administration’s odd connections to The Epoch Times, Falun Gong, Guo Wengui. Note: Erik Prince, worked for Hong Kong based security company, Frontier Services Group, led by Johnson Ko, where both Ko was a board member of Cambridge Analytica’s successor company, Emerdata, where Cambridge Analytica was used by Steve Bannon with funding from the Mercer Family – owners of Breitbart Media – to help Trump in 2016. Second Note: Tiawan was founded by the Right-Wing nationalist leader Chiang Kai Shek, and Taiwan was later headquarters to the World Anti-Communist League, which was an organization known for admitted ex Nazi war criminals.

Also, there is the Republican Party’s courting of Russia which is an autocratic society (this is similar to the Russian Anglo-American alliance in the Starship Troopers universe). We cannot also forget the rise of Right Wing Kookery as best seen in the social network surrounding pop figures such as Joe Rogan who has invited speakers that span John Birch-like paranoid Right Wingers such as Alex Jones, Theosophists, UFO believers, shamans, Jungian advocates such as JB Peterson….a lot of things which can lead to Neo Nazis.

Robert Heinlein had a syncretic political worldview. It seems contradictory if you get hippies but then also some radical pre-Alex Jones John Bircher’s liking your works. Inspired by both left wing and right-wing thought, his views could be considered 3rd Position or 3rd Way. He was influenced by Upton Sinclair’s socialism, the early basic universal income ideas (social credit) of C.H. Douglas, but the later adopted a more conservative, hawkish worldview. Heinlein was a libertarian in older age but sympathetic to socialism in his youth and he seems to have blended both, which is best viewed in the film adaptation of Starship Troopers in 1997 in my personal opinion. Heinlein to me represents the transition of Socialism’s acceptance in pre-WWII America, which in itself was a response to the Great Depression and embrace of earlier Progressive Era sentiments, to the post-WWII indictment of anything socialism, notably communism. This post-WWII shift of the late forties to early mid-fifties was a time where some very patriotic Americans who were socialist, shifted towards anti-socialist thoughts as hostilities arose with the USSR.

Heinlein’s emphasized personal responsibility and individual rights/liberty, yet did believe in the state, yet seems to have believed more in a populist as opposed to totalitarian type of state.

But Heinlein did support military and certain levels of government force when it comes to national defense and also “protecting us from ourselves” notably in regard to nuclear weapons. It seems confusing, but the best way to try to figure out “Heinlein-ism” as I might call it, is to play with terms such as calling it “right leaning, yet inclusive, global autocracy with an emphasis on the voluntaryist state that blends elements of both libertarianism and socialism, where the right of the franchise (voting) is granted to those willing to die to protect the body politic”. By Right leaning, I mean a devotion to the military and meritocracy, yet inclusive in that the meritocracy transcends notions such as race or nationality. [Note: There is a theory that neoconservatism was created by ex-Trotskyites, which has some basis in reality, but this theory seems more created by antisemitic paleoconservatives best typified by figures such as Pat Buchanan. See article by Bill King, 2004: https://enterstageright.com/archive/articles/0304/0304neocontrotp1.htm)

In 1959, Robert Heinlein published the science fiction novel, Starship Troopers. The book details a world after World War III where war veterans take over the governments of the world and establish a world federation based on meritocracy where in order to vote (the franchise) one must serve in the military. Per the novel form memory, the Anglo-American and Russian Alliance (which oddly reminded me of Trump’s aspirations with Vladimir Putin in previous writings) went to war with China, yet the Western powers essentially lost and settled with the Chinese at the Treaty of New Delhi. Yet, veterans were sprawled across the planet, and many having made it back to their homeland (with feelings of betrayal), found that modern society was decaying. A few veteran groups in order to combat violent crime and lawlessness started taking justice into their own hands (eerily harkening back to the post-WWI German veteran groups of Bavaria, the Weimar Republic, etc., which later evolved into the Nazis and their Brownshirts). Having established a quasi-governmental faction in their own right, this veteran collective eventually overthrew the scientists who were running western democracies. [Note: Blanquism is a form of putschism and it is interesting to note that the Nazis tried their own putsch with the Beer Hall Putsch in 1923]. Yet, these scientists attempted a Blanquist coup against the veterans in the Revolt of Scientists yet were beat. [ After that, the world slowly became a world federalist government ran by veterans, where in order to vote one must service the state with military service. Those who serve are called Citizens and those who do not are called Civilians. Citizens can vote, hold public office, etc. The new government that is established is the Terran Federation where differences of nation, race, gender, etc., don’t seem to matter but rather if a person serves in the military or does not, does matter. After this human world government is established, humans find themselves in conflict with an alien species, i.e., Arachnids from a planet called Klendathu.

In the 1997 film adaption by auteur director Paul Verhoven, is a satire of Heinlein’s presumably serious political treatise laid out in the 1959 book. Paul Verhoven and Ed Neumeier, who both worked together on the classic sci-fi film of Robocop (a scathing indictment of unfettered capitalism during Reagan’s nineteen-eighties), directed and wrote the 1997 film adaptation. The film has the main character Johnny Rico’s backstory (Juan “Johnny” Rico in the book) being based in …. Buenos Aires, Argentina. The film version expands upon the rights of Citizens such as the ability to go to college (at least for free), have children (possibly beyond a dictated limit), etc. Verhoven et al, cast good looking American 1990s TV drama actors of the Beverly Hills 90210, Melrose Place, MTV era. These fitness-like models were cast as a means of Verhoven paying nods (satirically) to the 1935 Nazi propaganda piece Triumph of the Will by Leni Riefenstahl. My opinion of 1997 film by Verhoven, for which I have been a fan of since I was a child in the fifth grade, is that Verhoven chose these very “whitewashed’ characters as a satire on the spreading of American capitalism, beauty standards, etc., i.e., a nod the colonizing and homogenizing effects of corporate culture, etc. It seems to be the case that the former United States had the most power within the Terran Federation’s establishment, so it’s already strong real-world culture laid the basis of this fictional government. Hence, American Vernacular English, its pop culture, etc., as is the case in our real world would have colonized the rest of the world.

Argentina is also important because it represents an extension of “whiteness” with the context of New World, post-colonial intersectionality. In our real world, the United States for example has a large swatch of the political base driven by fear of “white replacement” by way of immigration, challenges to traditional white male power, etc. This can be heard on cable news by figures such as Tucker Carlson, who dog-whistle to news watchers to inspire a sense of white fear, grievances, etc. Since globalism and cosmopolitanism are a part of our world and not going away, the definition of whiteness is moving the goalpost of what actually is white as a means of retaining statistical and numerical majorities. Hence, the United States as it undergoes the process of “Hispanicization” is shifting the definition of whiteness from the traditional definition of European, notably Northern and Central European (e.g., Anglo-Saxon stock), to include white Hispanics, where Latin America has its own complicated history with racial categorization (where one could say it is more fluid, yet also ironically rigid in certain ways since there is an aggrandizement of Eurocentric values as opposed to Indigenous, Afrocentric, multi-racial sentiments, etc.).

Yet, the film doesn’t address race and racism is not a part of the utopian world of Starship Troopers, nor is gender inequality. The world is a pure meritocracy.

But to expand on the Nazi influences that drove Verhoven’s satirical work, Argentina plays an important role because historically, Argentina as well as other South American nations harbored Nazi War criminals who were able to blend into the existing German and Italian immigrant populations. These Nazis used “rat lines” to enter Argentina, Chile, Brazil, Bolivia, etc., sometimes with the help of sympathetic Catholic priests assisting. For example, Klaus Barbie was active in Bolivia providing military training assistance to dictators involved in the early cocaine trade, which later assisted the powerful Medellin Cartel of Pablo Escobar via Roberto Suárez Gómez. Barbie was so emboldened that he had his own terror death squad in the country called the Fiances of Death and assisted in coup called the Cocaine Coup in Bolivia. Josef Mengle, the Angel of Death, was in South America. Otto Skorzeny (who later did assassinations for Israel’s Mossad as a means of not being hunted down and killed by them) even provided security detail to Argentina’s Juan Peron, husband of the famous Evita Peron. The infamous cult, Colonia Dignidad, created by Nazi and pedophile Paul Schäfer, was in Chile, and it is important to insert that Chile did have a pro-Nazi element with figures such as Esoteric Hitlerist Miguel Serrano. This cult has ties to the Pinochet Regime, which was a regime supported by the United States, corporations (such as the ITT Corporation, founded by Sosthenes Behn, which was later bombed by the radical Leftist Group, the Weather Underground for their participation in the overthrow of Salvador Allende), Richard Nixon all the way to Ronald Reagan, Henry Kissinger, Margaret Thatcher, and the CIA, as a means of hindering Left Wing movements on the continent during the Cold War.

Understanding issues facing African American Owned Businesses from Brand-Image to the Supply Chain

Applying Quality Management to African American Businesses

MGMT 691 Graduate Capstone Proposal

By Quinton M. Mitchell

M.S. Management (Operations Management) 2018

Embry-Riddle Aeronautical University (Worldwide Campus)

ABSTRACT

The purpose of this research paper is to (1) Explore any limitations to branding products or services created by African Americans as Black-Owned by conducting a literature review which analyzes scholars who argue for and against segregated economies, i.e., protected enclaves; (2) Understand consumer behavior differences between African Americans and other groups by understanding theories such as the Customized Communication Incongruity Theory by Arora & Wu (2012) and Socialization Theory by Ward (1987); (3) Explore how marketing and advertising affects African Americans and how diverse/positive marketing campaigns improves black success; (4) To show positive gains within the African American community but also to explore the hindrances to African American economic productivity such as higher insurance costs, lack of capital markets, sensitivity to economic conditions, etc., and (5) Discuss Supply Chain issues in African American businesses by using black-owned breweries for a test industry to implement concepts just as strategic alliances, best practices and/or to emulate practices such as those used by Japanese Keiretsu.

Table of Contents

Managerial Problem stated as a Research Question…………………………….…….5

Setting/Background……………………………………………………………………5-6

Research Activity……………………………………………………………………….6-7

Literature Review………………………………………………………………………7

To open the community or to close off the community?……………………………7-10

The underlying psychology of branding and marketing pertaining to African Americans…………………………………………………………………….10-12

Disparities between African American Owned Business and White Owned Businesses……………………………………………………………………12-16

How African Americans respond to brand image & issues regarding advertising and media portrayals…………………………………………………………………………….16-20

African Americans in the Supply Chain & the need for Strategic Alliances or Joint Ventures………………………………………………………………………………20-32

Is the Japanese Keiretsu model appropriate for African American Breweries? ….33-39

Figure 1. 2017 Top Black Owned Businesses by Black Enterprises…………….22

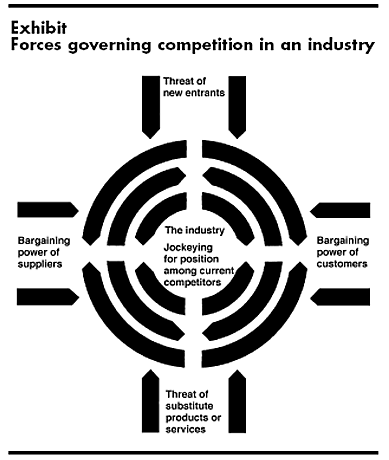

Figure 2. Michael Porter’s (1979) Five Force of Competition…….………………32

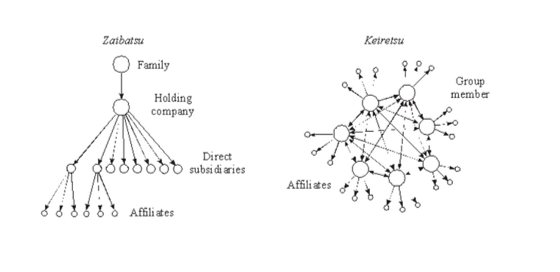

Figure 3. Zaibatsu vs Keiretsu by Yonekura (1985), cited by Grabowiecki (2012) …………33

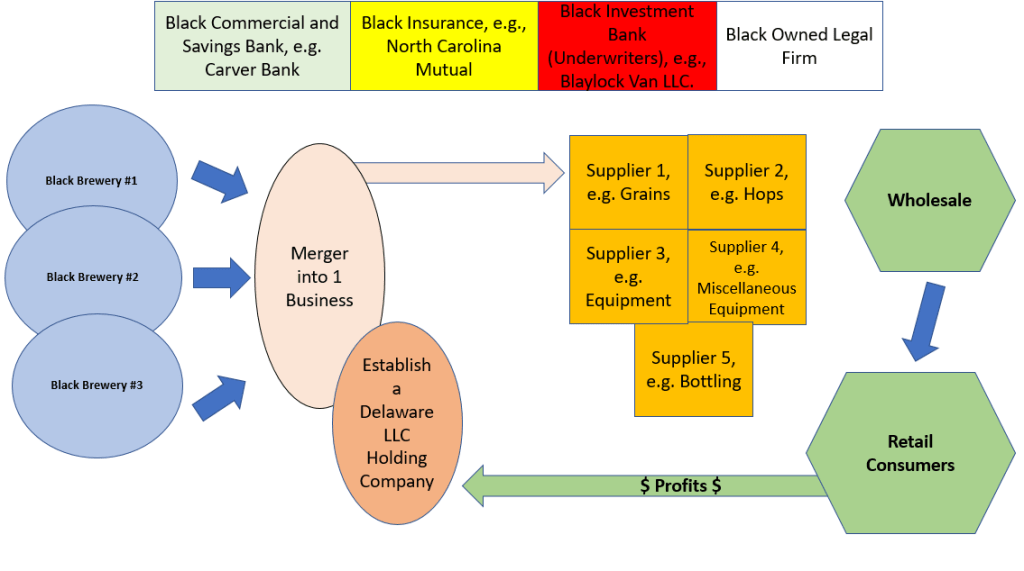

Figure 4. Theoretical Model for African American Brewery Consolidation………36

Keywords: African American, #business, #behavior

Managerial Problem stated as a Research Question:

Does the resurgence of labeling products as “Black Owned” has its limitations? Should African American owned businesses think bigger and take a risk by creating brand campaigns that targets a larger non-race specific consumer base? Should smaller African American owned firms join forces through concepts such as strategic alliances, joint-ventures, or even the Japanese concept of Keiretsu? Is it safe to view the black community as a singular entity, or does a complex intersectionality exists within the black-community, and, if so, which ideology, or which marriage of ideologies, is more effective at achieving sustained success for African Americans? In addition, can the establishment of a supply-chain network between African American owned businesses help improve visibility of brands, maximize economies-of-scale, improve service/item quality or value, and increase profitability?

I.Setting/Background:

African-American in business have a long history in the United States ranging from entrepreneurs or CEOs who have gone to build empires or sustain already established business empires; to running established firms who have made catered services and products towards African-Americans and the world at large, and the number of African-Americans winning managerial positions in name-brand American firms since the Civil Rights movement. Yet, Black-Owned businesses faces a plethora of issues ranging from access to credit, the risk-reward aspect of certain industries, and the fact that African-Americans, as with most Americans, have benefited positively from, while also being negatively impacted by the effects of globalism, the loss of labor protection, the hyper-competition of corporate multi-national companies.

In addition, Gillian B. White (2017) wrote an article that noted black CEO representation peaked in 2007 but has been slowly dwindling due to removal or retirement. As a result, I am arguing that black-owned businesses who market their products as “black owned” instead should market their products towards all consumers, regardless of the self-empowered notion of supporting black-owned businesses, because the level of product visibility and profitability will increase. Essentially, be black-owned, sure, and be proud of that, but market and win customers regardless of who they are. However, this paper is not an indictment of Black-Owned branding, but rather an argument that the call for branding products as such should of course be from a sense of empowerment, but not to the extreme of exclusivity which could have detrimental effects on capital accumulation and distribution of profits amongst the community. Why have one market, when you can compete with larger companies in multiple markets? To support Black-owned businesses and possibly improve the quality-of-life of certain African American communities, thinking bigger and expanding consumer bases can increase African American economic prosperity. For example, we know that Toyota is a brand of cars that is obviously made in Japan, and the brand is synonymous with quality, but the Japanese benefit from a clever branding strategy where the products does the talking for the culture. The goal of this paper is to provide recommendations to assist black-owned businesses, not from a stance of exclusion, but rather to further normalize products for all consumers regardless of race.

II. Research Activity:

A brief background into African American business ownership from a historical perspective will be presented. In addition, a historical view of race-centric marketing will be presented to strengthen the premise that race and marketing are often in unison. This historical perspective will lead up to my initial business problems facing the community and then I will follow up on conceptual ideas that could generate benefits. Giving dues when needed to the current landscape, I will then offer my recommendation for focusing on brand-image marketed towards a diverse consumer base, which in my opinion, can increase black economic output without labeling itself as “black-owned”, but if a firm decides to brand themselves as black-owned, which is justified considering the complex history of the United States, then there needs to be a strategic re-training of the thought process to challenge oneself to expand what new markets black Americans can or should participate in. Qualitative research will then be discussed to link the marketing of brands to the importance of the supply-chain.

Finally, a summary of the supply-chain as far as key aspects will be discussed and then I will construct a conceptual supply-chain or strategic alliance theory in which an African American business owner could formulate strategic ideas. The goal of this project is to emphasis strategic-thinking while loosely threading upon the quality management philosophies of early scholars such as Deming, Juran, and Crosby, to get Black-owned business owners to think more expansionist-minded, while simultaneously being inclusive towards all communities.

IV. Literature Review

A. To open the community or to close off the community?

Cummings (1999) presents a study comparing African American entrepreneurs conducting business in the ghetto’s protected- market versus the suburbs or larger Metropolitan Statistical Areas and argues that African American firms outperform when operating in larger non-segregated environments. Cummings (1999) provides a qualitative and quantitative study regarding the flaws of racially-segregated economies by touching upon the enclave-theory and protected market theory by referencing researchers such as Drake & Clayton (1945), Cummings (1980), and Light & Rosenthein (1995). In the study, Cummings (1999) states, “Although racial segregation may be a prime factor promoting ethnic and enclave enterprise, it simultaneously undermines business growth and development”. In addition, Cummings (1999) shares findings from Brimmer and Terrell (1971) who states that African American entrepreneurs who depend upon a segregated-protected market have high potential for failure. Moreover, when faced with desegregation and group dispersion, businesses that depend exclusively upon an enclave market are likely to fail (Brimmer and Terrell, 1971).

Rueben & Queen (2015) studied how African American owned businesses suffer adversely from unequal access to capital markets and the prevalence of institutional barriers. Although not universally appreciated, African Americans have a long history of entrepreneurial achievements against odds. African Americans are more likely to start a business, yet, are less likely to succeed (Rueben & Queen 2015). Rueben & Queen (2015) stated that the success of minority businesses to employ more workers and raise the productivity of workers is essential to U.S. economic growth, considering the U.S. labor forecasts (U.S. Bureau of Labor Statistics 2012, as cited by Rueben & Queen 2015), the 2025– 2050 outlook on the U.S. labor market is expected to grow slowly with most of growth coming from 55 million by minorities and immigrant workers. Further, despite these increases in the number of African American owned firms, African American entrepreneurs tend to participate in industry sectors with less capital requirements for start-up and expansion. However, some of these industries have lower revenue streams. Yet, when African American entrepreneurs operate in high revenue generating industries, their average annual revenue and average annual payroll per employee are significantly lower than their white counterparts (Rueben & Queen 2015).

The yearning to empower black businesses has led to a conflict in policy ideologies as presented by Cummings (1999). The enclave economy theory alludes to the positive outcomes associated with racially or ethnically segregated communities, but considering the criticisms presented by Tabb (1970) such as (1) smaller markets, (2) lower income consumers, (3) higher insurance rates, (4) inability to access credit, (5) higher rates of theft, and (6) limited access to capital, there are parties at be that wish to open the black community to larger markets but from the stance of community re-invigoration, yet not entirely from a segregated mentality. According to Cummings (1999), community-based development initiatives are activities inspired by or aimed at service social groups in a locality. In addition, community-based development initiatives also refer to those efforts organized by people who share a common urban geography (Blakely 1994).

Strategies that come from inwardly focused values and not economic realities are likely not going to make a competitive advantage (Barney & Hesterly, 2015, p 6). This touches upon my argument regarding the general trend in the growth – as far as a calling or social justice movement – of marketing products or services as Black-owned. There is nothing wrong with this, yet there are many assumptions and a diversity of ulterior motives that can occur when there is a calling for a segregate mentality. Such as, considering the social nature of human beings when classified, there can be a limit on the expressive modes – which can be profitable – that a group feels they can participate in. I call this a “culture-trap”, in which the standard or traditional culture is such a firm aspect of identity, that deviating to innovate for an individual, can have detrimental social and psychological effects. In addition, this “culture-trap” not only limits innovation, it can lead to issues such as brain-drain (when intellectuals leave the community in order to associate themselves with more supportive individuals), attrition (leaving the community), and the recycling effect of standard discourses when relating to issues effecting a community. Also, there have been clear examples of black-on-black business crimes or political corruption, in which the culprits have often used the calling for black segregation for their own financial and personal gains.

There seems to be a standard agreed upon set of values for African-Americans when consciously entering the business arena, i.e., a sense of liberation and self-empowerment, and although these yearnings are noble and arguably justified considering the sociopolitical and economic truths of African-American culture (slavery, segregation, red-lining, police profiling, etc.), yet the ultimate goal is, of course, to empower the group, yet it has to be based inevitably on an open-market, non-exclusive long-term agenda – with active but non-exclusive black participation – where products or services are focused on the bottom-line of profitability, penetrating new markets (both physical, i.e., foreign countries, but also unrealized cultural markets, i.e., cultural facets of American culture with black participation but that aren’t associated with black cultural as a whole) and the realization of a multicultural globalist reality based on a post-racialist idea or aspiration.

However, the claims provided by Cummings (1999), Rueben and Queen (2015), and Tabb (1970) are rebutted by Chaplain (2012) who argues that integration has destroyed the black economy. The black community lacked the requisite socio-cultural characteristics to develop a robust entrepreneurial tradition and, second, that integration, as an independent variable, destroyed black-owned business. Chapin (2012) studies the affects of government regulations which highly curtailed African American business growth and this provides more historical background on my study. Since insurance is a major part of entrepreneurship and running a business, Chapin (2012) study can shed light on the emotional reasons many African Americans are compelled to market their goods as black-owned and might give credence to the calling for black separatism. Yet, a major focus for business ownership growth and development in the African American community must be on the strategic expansion of the employer firms (Rueben & Queen 2015).

Chaplin (2012) seems to be of the vein of intellectuals who argue segregation as a benefit to African-Americans; however, Chaplin (2012) is sensitive to history, and only seems to be basing his premise on the fact that systemic injustice such as a society built on “white Affirmative-Action” had a detrimental effect on blacks, even though black communities formulated under this system and showed signs of progress. Yet, Cummings (1999) study on the undermining of business growth and Rueben & Queen (2015) study which shed light on the future growth of minority groups in the United States, I feel that there is a calling for creating a black-owned business mentality, yet, there is also the need for it not be exclusive. Essentially, we need more entrepreneurs and businesses owners, but the underlying motivation must be global and catering towards all people.

B. The underlying psychology of branding and marketing pertaining to African Americans

Jeffrey Steven Padoshen (2008) presents a compelling study into how African Americans value and apprise goods based off unique characteristics of their community. As “minority” groups such as African Americans and Latinos grow in overall proportion to America as a whole, particular attention must be placed on the understanding of their consumption characteristics (Padoshen, 2008). Padoshen (2008) presents a study that investigates word-of-mouth and brand loyalty within the context of durable-goods purchases in the African American community to see if there are effects on purchase decisions when a supplier was at one time linked to the slave trade, and if there’s a preference for purchasing products which come from black-owned companies. Padoshen (2008) provides a historical background into African American communication by referencing Thorp & Williams (2001) who argued that African American uprooting from their African homeland destroyed the means of communication. Further, Padoshen (2008) references Harris-Lacwell (2004) & Gothard (2001) who argued that oral-storytellers remedied these severed means of communications (Thorp &Williams, 2001) within the black community. Padoshen (2008) references Gothard (2001), Thorp & Williams (2001), & Harris-Lacwell (2004), & Miller & Kemp (2005) many times throughout his insightful study. Both Gothard (2001) and Miller & Kemp (2005) defined word-of-mouth communication within the context of the African American community – a major part of African American culture – as having four (4) distinct elements, which is trust, respect, open-voice, and black-to-black communication.

According to Padoshen (2008), African American culture is one in which greater distinctions are made between outsiders and insiders compared to Anglo-American culture (de Mooij, 1998) and significant weight is attached to personal qualities. For many African Americans, premium brand names and symbols are mechanisms that reflect the hard and long portrayal of higher aspirations (Miller and Kemp, 2005). Further, Miller & Kemp (2005) speaks into how African-Americans favor brand-names because it is reflecting a “badge” or “badge of honor”, particularly for a group who was largely relegated to be an outsider, thus, wearing brand-names helps to include these people into the overall larger culture. In addition, Padoshen (2008) states that African Americans have indicated that when purchasing automobiles, brand nameplate, looks and style are more important in their purchase decision than safety when compared to Anglo Americans (Packaged Facts, 2006).

Padoshen (2008) references one of his prior studies (Padoshen & Hunt, 2006) to support his claim that historical treatment of African Americans, similar that of Jews who suffered under the Holocaust, can have generational effects when buying products from sources who are equates with supporting or benefiting from the systemic injustices that kept that their people subjugated. The most important finding of Padoshen (2008) finding is that, African Americans indicate that they are no more trusting of the advice they receive in comparison with that of Anglo Americans. Padoshen (2008) research is an exceptional example of the dilemma facing most African Americans in my opinion, which is that studies – even if objective without any sort of racial bias – assumes a distinct racial and sociopolitical characteristic than that from the larger culture they are technically a part of. This bias, even if assumed on noble grounds to prevent an issue such as systemic injustice, can never lead to a full understanding of human nature. Essentially, we can define a group up to a point, but can never fully know a group, or even a group understanding itself entirely, which isn’t a bad thing – from a business perspective, this is new unrealized markets and ways towards profitability.

C. Disparities between African American Owned Business and White Owned Businesses

Tang & Smith (2013) conducted a study that researched African American business disparity in comparison with White-owned businesses regarding market segmentation, product differentiation, and competition, but their findings suggested that the difference was not statistically significant. Tang & Smith (2013) studied the largest African-American owned employer firms from 1998-2008, as published in Black Enterprise Magazine, in which businesses on the list must be at least 51 percent African American-owned if a private company, or African Americans must own at least 51 percent of the controlling shares if the company is publicly traded and be willing to voluntarily provide financial data. Yet, Tang & Smith (2013) admits a bias in their research as far as selection of candidates from the Black Enterprise Magazine, in that some of the firms on the list may be “front companies”, in that they are non-African American owned but registered as such and that certain actual African-American owned firms may not have given up financial data to maintain a non-disclosure position. From personal experience in government and corporate procurement, where seeking minority, woman-owned, or general small (no-racial assignment) businesses is a goal, I have found this misrepresentation of classification as something endemic in the procurement field.

Tang & Smith (2013) utilized a contingency (environmental)-view to study Black business disparity when compared to White-owned businesses, in which they cite Aldrich’s (1979) definition of a contingency-view as explaining variations in firm performance from the interaction of the organization and environment, in which environments affect firms through the process of making or withholding resources, and the top three environmental contingencies are complexity, volatility, and munificence. Munificence is defined as very liberal in giving or bestowing or characterized by great liberality or generosity (Munificent, n.d.). Tang & Smith (2013), summarizes their utilization of the contingency (environmental influenced)-view, by saying, “When the rest of America catches a cold, Black America gets the flu. In other words, declines and dips in environmental variables like income, GDP, and labor supply will have a greater negative impact on black businesses. The number and type of contingent environmental factors able to influence the performance of established African American firms is undoubtedly numerous.”

A large motivator in conducting their research, Tang & Smith (2013) cited Fairlie & Robb (2012) who stated that it is estimated that closing the revenue gap between minority and non-minority owned businesses would add $2.5 trillion to the US economic output, creating 11.8 more jobs in America; Fairlie & Robb (2008) who stated that performance disparity might stem from issues of start-up capital, owner’s education level, and prior business experience, and Keollinger et al (2007) who stated that African-Americans have lower personal wealth, greater difficulty in obtaining financing, less education, and lack of entrepreneurial legacy. Further, Tang & Smith (2013) cited research by Puryear et al. (2001) which found that African-American owned businesses were the only minority group to report medium gross sales significantly lower than their white comparison sample, and African-American businesses where the least success as rated by their owners. In addition, Tang & Smith (2013) states that some of the studies pertaining to performance disparity between African-American and majority-owned firms, focus almost exclusively on sale proprietors or entrepreneurial firms undergoing the start-up stage (e.g. Buckley, 2002; Puryear et al, 2001; Richtermeyer, 2002); However, the focus on more established business will likely shift from overcoming liability of newness and survivability to concepts such as market segmentation, product differentiation, and competition as the business moves through the typical life-cycle (Hofer, 1975 – as cited by Tang & Smith, 2013).

Overall, Tang & Smith (2013) concluded that (1) the complexity and volatility associated with one of the most difficult US business environments since the 1940s (the Global Recession, in my own words) may increase the performance disparity between established African American and White-owned firms; (2) that existing knowledge about African American entrepreneurial firm performance may not transfer to larger, more established African American businesses; (3) their findings do not suggest that emerging African American firms should avoid entering complex and volatile industries;(4) emerging African American businesses often operate in industries that are more favorable, marked by less complexity and volatility such as construction, wholesale trade, and manufacturing (US Department of Commerce Minority Business Development Agency, 2011), but these industries are characterized as relatively low growth industries (Tang & Smith, 2013); (5) a “strategic choice” approach would imply that despite unfavorable industry characteristics, African American businesses may be able to actively shape their future and control their environment (Child, 1972), responding to threats and opportunities created by environmental change by altering organizational strategies in ways that enhance performance (Pfeffer and Salancik, 1978; Porter, 1980). The task for African American businesses then becomes developing the capabilities or distinctive competencies needed to overcome isolating mechanisms and mitigate industry conditions (Tang & Smith, 2013).

It is on black community-leaders to be open-minded (challenging the culture-trap I referred to earlier and opening new ways of thinking, while community member simultaneously keep open-minds as to not be lead to narratives which might not account for the entire truth) considering Thorps & Williams (2001) claim that authentic leaders who “tell it like it is” have strong community influence as cited by Padoshen (2006); in the African-American community, greater distinctions are made between outsiders and insiders with weight attached to personal qualities (de Mooji, 1998 – as cited by Padoshen, 2008); brand names and symbols are signifiers of higher aspirations and are considered badges-of-honor (Miller & Kemp, 2005 – as cited by Padoshen, 2008), so much so that safety – at least relating to automobile purchases – is largely a non-impactful decision (Packaged Facts, 2006 – as cited by Padoshen, 2008); African-Americans are no more trusting than Anglo-Americans (Padoshen, 2008); closing the revenue-gap between whites and blacks would add $2.5 trillion to the US economic output (Fairlie & Robb, 2012 – as cited by Tang &Smith, 2013); African-Americans have lower personal wealth, greater difficulty in obtaining financing, less education, and lack of entrepreneurial legacy (Keollinger et al, 2007 – as cited by Tang & Smith, 2013); more established firms will shift from survivability and newness to market segmentation, product differentiation, and competitions (Hofer, 1975 – as cited by Tang & Smith, 2013); information on African-American start-up and entrepreneurial performance many not reach established African-American firms, the Global Recession had a negative impact on the African-American community, and African-American firms often operate in less volatile or complex industries with relatively slow growth (Tang & Smith, 2013; US Department of Commerce Minority Business Development Agency, 2011), yet, these unfavorable characteristics – speaking to volatile and complex markets – may be able to actively shape African-Americans futures (Childs, 1972 – as cited by Tang & Smith); the black church, barber-shop and beauty salons and other informal settings fosters open interaction (Gothard, 2001; Harris-Lacewell, 2004 & Miller & Kemp, 2004 – as cited by Padoshen, 2006 and 2008).

V. How African Americans respond to brand image & issues regarding advertising and media portrayals

Kristen Bialik (2018) of the Pew Research Center, noted that (1) more than 40 million blacks live in the United States, making up around 13% of the nation’s population according to 2016 Census Bureau estimates (US Census Bureau, 2016); (2) The share of blacks ages 25 and older who have completed four years of college or more has also roughly doubled during that span, from 12% in 1993 to 24% in 2017 (United States Census Bureau, 2017); (3) There were 4.2 million black immigrants living in the U.S. in 2016, up from 816,000 in 1980, according to a Pew Research Center analysis of census data, and recent growth in the black immigrant population has been fueled by African migration at 39% of the overall black immigrant population in 2016, up from 24% in 2000, but about half of all foreign-born blacks (49%) living in the U.S. in 2016 were from the Caribbean (Lopez & Radford, 2017, as cited by Bialik, 2018); (4) the wealth gap between blacks and whites decreased among lower-income families but increased among middle-income families. The Great Recession of 2007-2009 triggered a stark decline in wealth for U.S. families and further widened the already large wealth gap between white and black households (Konchhar & Cilluffo, 2017); (5) There has been a steady increase in the share of Americans who view racism as a big problem in the U.S. – especially among African Americans since 2009, when Barack Obama was elected. In 2017, about eight-in-ten blacks (81%) said racism is a big problem in society today, up from 44% eight years prior. By comparison, about half of whites (52%) said racism is a big problem in our society, up from 22% in 2009 (Neal, 2017), and (6) An overwhelming majority of blacks (92%) say whites benefit at least a fair amount from advantages that blacks do not have. This includes nearly seven-in-ten blacks (68%) who say whites benefit a great deal. By comparison, 46% of whites say whites benefit at least a fair amount from advantages in society that blacks do not have, with just 16% saying whites benefit a great deal (Oliphant, 2017).

Dimofte, Johansoon, & Bagozzi (2010) conducted a study based off a survey sample pool from an online panel of more than three million consumers in the U.S. where the pool was stated as being generally reflective of the overall American consumer base – seeking equal representation among factors such as gender equality and educational attainment, although the sample relating to African Americans had more African American female respondents and when relating to Hispanic Americans had more younger male Hispanic respondents. Dimofte, Johansoon, & Bagozzi (2010) then compared global brand recognition among diverse ethnic groups by basing their main concerns on Phinney’s (1996) definition of ethnicity and his first aspect of ethnicity which is cultural values, attitudes, and behaviors of groups.

Dimofte, Johansoon, & Bagozzi (2010) drew conclusions based from survey data analysis and a structural equation model which suggests that associations with global brands as a general category vary across ethnic groups, such as Caucasian consumers showing less of an appreciation of global brands, whereas African Americans and Hispanics show similar patterns to those of prior research such as that of O’Hara (1987) who suggests African Americans & Hispanics have more similarities to markets in lesser developed nations; the research of Alden, Steenfamp, and Batra (1999) who posited that most global brand findings are based on cross-national samples and that the global brand effect is particularly strong in less developed countries, and the research of Darley & Johnson (1993) who presented that African American marketplace behavior and attitudes toward advertising reflect those observed in less developed countries in Africa and Asia, including more positive attitude towards globalization. Furthermore, Dimofte, Johansoon, Bagozzi (2010), states, “U.S. consumers tend to be more diverse than in most mature market economies, with large ethnic-based market segments”, thus enabling Dimofte, Johansoon & Bagozzi (2010) to identify potential differences between Caucasian Americans and ethnic minority market segments.

Dimofte, Johansoon, & Bagozzi (2010), understanding the complex issues with gathering, organizing, defining, and measuring global brand research, admits that research on global brands is more limited (Keller, 2007). Minority groups are young on average than the rest of the U.S. population and thus are more attractive to marketers (Dimofte, Johansoon, & Bagozzi 2010). Further, O’Hara (1987) & Pitts et al. (1989) as cited by Dimofte, Johansoon, & Bagozzi (2010) states that African American segment has long been of special interest to marketers, with products adapted for their special needs, especially in cosmetics, personal care products, food, and print media.

Dimofte, Johansoon, & Bagozzi (2010) indicates that it is generally accepted that consumption behavior, especially a conspicuous brand choice, is to some extent reflective of individual identity and social aspirations, thus, choice of brand especially for product categories with social visibility, constitutes an expression of identity and achievement, or, in other words, self-expressive markers and identity forgers considering global-brands are well-known and widely recognized, which thus makes them more adept and effective at service a social function. Overall, Dimofte, Johansoon, & Bagozzi (2010) summarizes African American and Hispanics generally favored globalization; Caucasians did not think that global brands had higher quality, but Caucasians did feel global brands had consistent quality; African Americans and Hispanics perceive the prices of global brands as higher, but all three groups show a cognitive consistency that global brand is a relevant attribute, and that African Americans and Hispanics favor higher quality although the sale of higher quality goods are best marketed when the aspiration-factor is implied and not emphasized.

Arora & Wu (2012) conducted a study that researched how positive and negative stereotypes were found to impact ad-evoked feeling and brand equity, by theorizing that stereotypes through print advertising generates Customized Communication Incongruity. The results of the study conducted by Arora & Wu (2012) concluded that for positive stereotypes, both males and females prefer positive stereotypes, and positive stereotypes influenced ad-evoked feelings that influenced brand equity for both genders. Further, the Arora & Wu (2012) study concluded that brand loyalty and perceived quality dimensions of consumer-based brand equity were not significantly impacted by negative ad-evoked feelings, with males more agreeable of negative stereotype advertising than females, but both genders still generated negative ad-evoked feelings. The simplest way to summarize Arora & Wu’s (2012) theory of Customized Communication Incongruity, is when an individual sees an advertising that results in a mismatch or distortion of values or expectations. Thus, their study relating to racial stereotype-based advertising is meant to study how people react to media that is arguably stereotypical, and whether this response has effects on brand-value.

The Customized Communication Incongruity Theory by Arora & Wu (2012) builds off schema-based research provided Leoff (2002) who suggested that ads that do no match advertising expectations are more likely to draw consumers’ attention and proceed more extensively than ads that match advertising expectations, thus providing a way for brands to stand out. Advertisers have a strong influence on shaping consumer perceptions as advertisements can either help eradicate the negative perceptions of African Americans, or they can facilitate pervasive stereotypes, which may increase racism (Arora & Wu, 2012). In other words, ad campaigns that break stereotypes can spur continued interests. Arora & Wu (2012) cited Stevenson & Swayne (2011) whose research suggested that as of the late 90s, there were a small percentage of black models used in in magazine advertisements when compared to the general population. Further, Arora & Wu (2012) cites Cohen & Garcia (2005) who suggested that application of negative stereotypes of a racial group, with media as a reinforcement tool, brings discrimination and stigmatizations to the front, and media when based on stereotypes can have adverse effects to self-esteem, self-efficacy, and even level of achievements.

Fortenberry & McGoldrick (2011) conducted a study on outdoor advertising regarding African Americans and found that there are differences between white and black consumers’ receptiveness to outdoor billboard advertising. These differences are highly significant across each of the items within the scale of receptiveness, measuring awareness, influence on patronage, information conveyance, and overall attitude toward the medium. The receptiveness difference is at least in part a function of education and income, and the differences lose their significance only at the highest levels of both. Maybe surprisingly, the affluent black consumers without college education show higher levels of receptiveness (Fortenberry & McGoldrick 2011).

Yet, Fortenberry & McGoldrick (2011) cites Ward’s (1987) socialization theory, in order to find reasons for why college-educated affluent blacks mimic less receptiveness to billboards similar to that of their white counterparts and concluded that education socializes people to be more critical away from family and personal social bonds, and that the increased income generated by furthering education helps people migrate to areas where billboard advertising isn’t as common or accepted. Lastly, Fortenberry & McGoldrick (2011) cites Morris (1993) and Yoon (1995) who summarized that Black Americans demonstrated a greater degree of openness in discussing the influence of billboards within their society and supported the views that they have strong interest in material possessions.

Yuki Fujikoa (1999) conducted a study to show the effects of vicarious contact via television on stereotypes of African Americans among White and Japanese college students, in which the study provided some evidence that television messages had a significant impact on viewers’ perceptions when first-hand information was lacking. The study suggests that perceived positive portrayals of African Americans on television are effective in reducing negativity (Fujikoa 1999). It is more effective to reduce negative stereotypes of African Americans when we interact with many different African Americans who display counter-stereotypical behavior than when we interact with intimate African American friends (Fujikoa 1999). Since television can show a variety of positive African American models to a relatively large audience, television seems to have a great potential for stereotype reduction. Fujikoa (1999) cites Berg (1990) who stated that stereotypes are not necessarily negative, but they can destructive or bad when used by the dominant group to underscore majority-minority differences or to make some other (e.g. ethnic minority) groups inferior. Further, Fujikoa (1999) cites Berg (1990) who stated that interracial contact helps develop a mutual relationship between members of the two ethnic groups (e.g. White and African Americans), and we may expect an improvement in racial attitudes.

VI. African Americans in the Supply Chain & the need for Strategic Alliances or Joint Ventures

Yet, to reiterate, Rueben & Queen (2015) more than half of the 106,566 African-American (AA) owned employer firms (67,665 or 63.5 %) participate in only 5 of the 22 major North American Industry Classification System (NAICS) sectors: (1) Health Care/Social Assistance, (2) Professional/Scientific/Technical Services, (3) Retail Trade, (4) Administrative Support/Waste Management, and (5) Construction, yet these 5 industries are included in the top 10 revenue generating industries for all firms.

Black Enterprise Research (2016), of the organization Black Enterprise, which defines itself as a total media firm whose goal is providing premier business, investing, and wealth-building resources for African Americans, presented the following list of top-performing African-American firms.

Figure 1 – Black Enterprise Research List of Top African American Businesses by Revenue (2016)

According to the United States Census Bureau (2012) the North American Industry Classification System (NAICS) is the standard used by Federal statistical agencies in classifying business establishments for collecting, analyzing, and publishing statistical data related to the U.S. business economy. NAICS was developed under the auspices of the Office of Management and Budget (OMB), and adopted in 1997 to replace the Standard Industrial Classification (SIC) system (U.S. Census Bureau, 2012). NAICS codes from personal experience are important because from a government procurement standpoint, many solicitations are issued based on NAICS codes, so the more a firm has diverse NAICS codes, the more chance they have at being discovered by government contracting agencies, but also the higher possibility of the firm relating their company’s unique products of services to that of government issued solicitations. For example, while in the United States Air Force, while serving with the 325th Contracting Squadron at Tyndall Air Force, Florida, when soliciting for commercial items, equipment, commercial construction, IT products etc., I was required to find sources based on NAICS codes. If a firm didn’t have a NAICS code listed under their profile either in the Government-Point-of-Entry called Federal Business Opportunities or through another market research tool such as the Small Business Administration’s Dynamic Business Search (http://dsbs.sba.gov/dsbs/search/dsp_dsbs.cfm), then than firm might be overlooked.

A brief skim over the top twenty firms as provided by Black Enterprise Research (2016), it seems to align to the research provided by Rueben & Queen (2015) with Health Care/Social Assistance, Professional/Scientific/Technical Services, and Retail Trade (which I will caveat as including automotive parts sales and food services) being represented. Yet, from the view of any onlooker in this paper, there is something missing: there are no actual large name, visible brand names, or brand-name manufacturers on the list, i.e., Ford Motor Company, General Electric, Starbucks, etc.

This leads back to issues facing African-American firms such as (1) unequal access to capital markets and the prevalence of institutional barriers (Rueben & Queen, 2015), (2) issues of start-up capital, owner’s education level, and prior business experience (Fairlie & Robb, 8008 – as cited by Tang & Smith, 2013), and the reality of a historical treatment in which African-Americans entered the business arena when the United States was already on its way to de-industrialization and globalization, i.e., the cost and liability of being a large manufacturer were disadvantageous to African-Americans. So, it seems that African American firms are highly active either as suppliers within already established supply-chains that supplements larger manufacturers – either as multi-year contract suppliers through agreements with larger firms, or as stand-alone units that are smaller than more visible corporate entities such as Fortune 500 companies. African-American firms can generate profits, but as far as dominating markets in comparison with standard Fortune or S&P 500 firms, it seems that African-American firms are used by these firms to maintain smaller demographic specific markets (for example, Johnson and Johnson owing a firm that sells black hair-care products) or helping achieve their larger strategic-goals by making including them as suppliers within their supply-chains.

This insinuates that (1) winning long-term contracts with larger firms is vital and (2) overcoming capital-constraints and operating in a globalist reality is something that needs to be realized by Black business owners. The second statement, can be fulfilled either through government financing programs, such as grants, loans, or obtaining government contracts; private financing from large banks who have a goal of supporting minority-owned business; private financing through black-owned banks, such as Carver Federal Savings Bank (https://www.carverbank.com/), who theoretically can target or work with viable black-owned firms to issue credit for start-up firms or established firms while simultaneously expanding their reserves, and/or luring in foreign-direct investment through acceptable financial institutions, particularly in developing regions such as Africa in which the majority of black immigration to the United States are coming from.

Whitfield & Farrell (2010) conducted a study that suggested that African American executives were less likely to perceived constructive dimensions of organizational culture. Whitfield & Farrell (2010) references Gomez-Mejia & Palich (1999) who stated that a diversity inclusive corporate culture is said to improve innovation and adaptiveness in heterogeneous market segments faced by international companies, and Crook et al (2008) who stated that building diverse supply-chains is seen as an additional effective means of increasing a firm’s performance similar to employer diversity. Additionally, Whitfield & Farrell (2010) references the United States Small Business Association (2001) who stated that minority-owned businesses have been a growing segment of the U.S. economy, nearly doubling as a percentage of the economy from the mid-1990s to early 2000s, and Eroglu, Green Thornton, & Bellenger (2001) who stated that this growth has become a business necessity.

Whitefield & Farrell (2010), concludes their research by stating, “There is some cause for optimism among these findings of perceptual differences. Between the non-minority buyers and the African American supplier CEOs the significant difference is that these suppliers see the buyer culture as less constructive. The African American CEOs see less passive defensiveness and less aggressive defensiveness than the buyers. For the African American, the views are different from Caucasians but not extreme or opposite. The Hispanic minority CEOs perceptions are more divergent from the perceptions of Caucasian buyers. For the Hispanic supplier CEOs, the buying organization culture appears defensive to cultural diversity.” In summary, regardless of what color the supplier or buyer is, when purchasing firms that are white-owned or black-owned, or for suppliers who are black-owned or white-owned, there is an easier framework to conduct business.

Selecting a specific industry and developing a specific-supply chain model for a firm is theoretical for this paper. Speaking for the need to implement standard Supply-Chain concepts such as Enterprise Resource Planning systems (SAP, Peoplesoft, Oracle), utilizing third-party logistic firms, speaking to supply-chain concepts such as Statistical Delivery rates or Quality control, or issues of warehousing, doesn’t necessarily offer coherent strategies for improving African-American firms. Instead, the research I have pulled insinuates that African-American firms are profitable yet tend to operate in the role of supplier to larger firms, considering the capital constraints are often to daunting to be an effective large scale manufacturer or conglomerate, and/or African-American firms tend to operate as stand-alone entities functioning within the larger economy and catering towards customers either on a non-exclusive first-come first-serve basis regarding their products (restaurants, logistics companies, healthcare services, or IT services), or operation on an exclusive-basis in which products or services are catered towards unique cultural taste such as barbershops, cosmetics, etc.

For African-American owned firm to reach economies-of-scale – considering the institutional barriers, capital constraints and business realities – strategies such as strategic alliances or joint-ventures between African-American owned firms could be implemented to join forces thus facilitate maximizing economies-of-scale. This strategy could reconcile the realities of the modern American business environment which is defined by expensive labor costs, the potentiality of collective-bargaining or unionism, and free-trade in a globalist reality. By developing strategic alliances or joint-ventures between African-African firms, even if firms are unrelated to each other as far as the products or services they offer, this could help pool human and financial capital, limit tactic knowledge, facilitate mutual marketing of each other’s products, etc. Essentially, since African-Americans were introduced to the free-market of the mid-to-late twentieth century, when being a stand-alone manufacturer was becoming a more daunting task, African-American firms can combine forces, under single incorporation, in order to have more a visible and real impact on the economy. Former separate CEOs could then serve as board-members and by pooling together each other’s profitability under one roof this could help this theoretical firm get public financing which would then create more capital to expand into Afro-centric markets but also markets that aren’t racially exclusive. This compounding effect would not only have a social effect on the general public because people would be able to associate a large-scale firm with African-American success but could help create capital that could be targeted on innovation that would otherwise be non-existent if firms operated as stand-alone units.

For African American firms to reach the level of profitability that can have a global effect but also a community-empowering effect, the goal must be about winning a competitive advantage. A firm has a competitive advantage when it can create more economic value than rival firms (Barney & Hesterly, 2013, p 8). In addition, Barney & Hesterly (2013) states that competitive advantage is when a firm creates more economic value than rival firms, and economic value is simply the difference between the perceived benefits gained by a customer that purchases a firm’s products or services and that full economic cost of these products of services. In order words, the customer must think a product or service has more value (Benefits > Cost = Value) than that of competitors, but the firm is liable of sustaining this perception of higher value by providing quality services or products.

To achieve competitive advantages, not at the expense of other Black-owned businesses, African American firms may benefit through strategic alliances, joint-ventures, or the Japanese concept called Keiretsu. In a joint venture, the companies start and invest in a new company that is jointly owned by both parent companies (Marzec, 2016). A strategic alliance is a legal agreement between two or more companies to share access to their technology, trademarks, or other assets. A strategic alliance does not create a new company (Marzec, 2016).

Regarding the concept of Keiretsu, Minor, Patrick, & Wu (1995) referenced both The Economist (1991) which stated that the most inclusive definition for keiretsu is that they are families of firms with interlocking stakes in one another, and Cohen (1985) who stated that keiretsu were encouraged by guidance, tax incentives, financial guarantees, direct subsidies, and protection from foreign competition. Further, Minor, Patrick, & Wu (1995) explains that keiretsu were the descendants of the pre-war zaibatsu, which were vast mining-to-manufacturing conglomerates based on the banking system, but the zaibatsu were disbanded, yet restriction on cross-shareholding were lifted; One of the unique aspects of keiretsu is that from 20 per cent to 40 per cent of stock is owned by member companies of its own keiretsu, and 60-80 per cent of the keiretsu stock is never traded; Horizontal, or bank-centered, keiretsu bring companies together to work on long-term projects that would be financially impossible for a single firm. These projects often turn out to be highly profitable because foreign competitors cannot take advantage of such partnerships where antitrust laws are more stringent (Boarman, 1993), and the vertical, or supplier keiretsu, forms when major manufacturers, such as an automobile maker or manufacturer of household electrical appliances, contract with suppliers for sole sourcing in exchange for production agreements excluding other buyers. Japan’s keiretsu, Korea’s chaebol, and Mexico’s grupos have played an important role in their countries’ development since the Second World War. These industrial conglomerates, bound by family ties, long-standing friendships, common ownerships and interlocking directories, and closely allied with their national governments, have spawned and linked industrial clusters in agriculture, minerals, basic industry and manufacturing – raising national productivity and their nation’s international competitiveness (Minor, Patrick & Wu, 1991).

Regardless of the organizational structure of Black-owned firms there always needs to be an emphasis on quality. High-quality goods and services can provide an organization with a competitive advantage (Evans & Lindsay, 2014, p 4). Further, Evans & Lindsay (2014) summarizes the Three Gurus of Quality Management – Deming, Juran, and Crosby – by saying, “Despite their significant differences to implementing organizational change, the philosophies of Deming, Juran, and Crosby are more alike than different. Each view quality as imperative in the future competitiveness in global markets; makes top management commitment an absolute necessity; demonstrates that quality management practices will save, not cost money; places responsibility for quality on management, not workers; stresses the need for continuous, never-ending improvement; acknowledges the importance of the customer and strong management/worker partnerships; and recognizes the need for the difficulties associated with change the organizational culture” (p. 64).